Let’s talk about something most of us are quietly guilty of: postponing our financial sanity until some mythical future day when our salary magically multiplies by ten.

You know the drill. You nudge someone—maybe even yourself—about saving or investing. And you get the classic line:

“Dude, I don’t even earn enough yet. I’ll start budgeting when I make real money.”

Fair enough. If you’ve just started working, your salary probably looks like pocket money in a Bollywood star’s wallet. You’re busy figuring out how to survive until the next paycheck without resorting to Maggi for every meal. It is true that you’re likely running at a deficit.

But here’s where it gets interesting: this isn’t really about the money. It’s about the habit.

When I first started dabbling in accounting (and by dabbling, I mean struggling to use Tally without accidentally deleting everything), my salary was ₹5,694 after TDS. Yep. I remember that number like it was tattooed on my forehead.

And no—please don’t think I was some frugal wizard who invested every paisa wisely. I spent plenty on nonsense and dubious “hobbies.” But I’d also bought a self-help book off Andheri station, hoping to learn how to track the tiny trickle of cash I called an income. Not because it was a lot, but because I suspected the skill would matter someday.

Spoiler: It did.

You see, money works a lot like water. If you don’t know how to turn the tap on and off, you’re going to flood the bathroom or die of thirst. And with cash, you don’t even get to see the puddle forming under your feet until it’s too late.

Yet most of us don’t start practicing these basic money moves until we’re in our twenties—when the stakes are higher, the mistakes more expensive, and the embarrassment more real.

There’s this lovely myth floating around: “Once I start earning big, I’ll figure it all out.”

Let me break this gently: if that were true, every government would be a shining example of financial prudence. But no—most of them collect mind-boggling tax revenues and then somehow blow it all on free TVs and equally questionable schemes.

Because if you can’t manage ₹10,000, you sure as hell won’t manage ₹2,00,000. The game changes—more money means more decisions, more options to screw up, and more sophisticated traps to fall into.

That’s why lottery winners end up broke faster than you can say “KBC.” They never learned to handle the flow, so when the tank showed up, they turned on every tap—long showers, garden hoses, and a full-blown water park.

Please don’t be that guy.

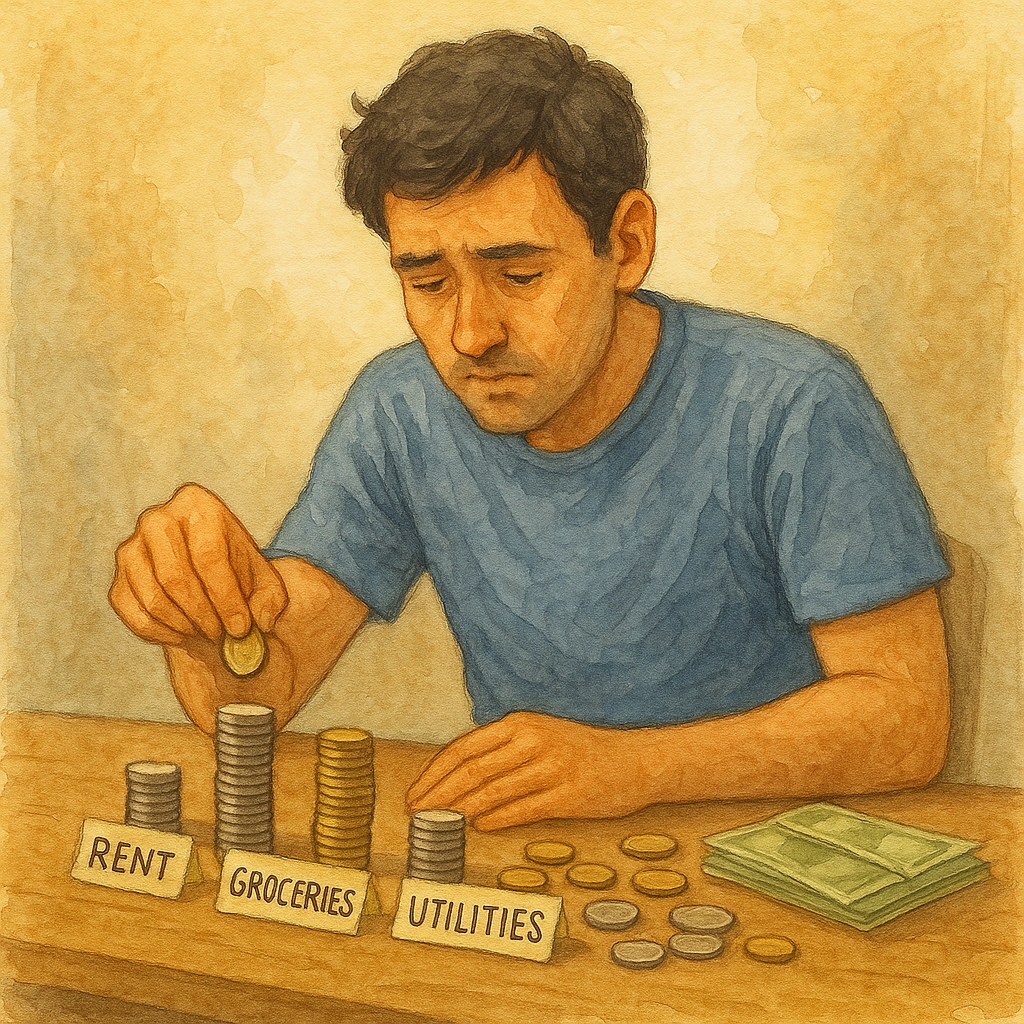

Don’t postpone your financial education because you think you’re “too early” or “too broke” to need it. If anything, that’s the best time to start. Because it’s never about the amount—it’s about the habit.

Look at every rupee as a percentage. Whether you’re budgeting ₹500 for vegetables or ₹5,000, the principle stays the same: you decide what share goes where. That habit, once ingrained, scales up with your income—and that’s when the magic happens.

And yes—once you hit your big milestones, you can tweak, reallocate, or splurge a little. But you’ll do it intentionally, not because you’re lost.

So if you’ve been waiting for some grand signal to start—this is it. The best time to begin was yesterday. The next best time? Right now.

Stop scrolling. Pick up that personal finance book. Open that savings account. Start that tiny recurring deposit.

Don’t worry about the returns yet.

Just start the habit.

Because that habit will take you places your paycheck alone never could.